Warren Buffett Does Not Understand a Crucial Point About Climate Risk

Billionaire Warren Buffett’s latest annual letter to shareholders dismisses the risk of climate change to his investors. And yet he never mentions that last year he spent $240 million buying another chunk of Canadian tar sands giant Suncor, upping his overall bet on the dirtiest liquid fuel to $1.1 billion.

Buffett also sings the praises of renewable energy in the letter, while omitting any mention of his company’s numerous efforts to kill solar energy in the Western United States. I’ll discuss that in a later post.

Buffett is undoubtedly one of the most successful investors in the world, though he still suffered terrible losses from underestimating the full risks of the Great Recession and housing bubble. Also, the stock of his company, Berkshire Hathaway, has actually underperformed the S&P 500 over the last five years.

In his 2016 letter, Buffett responds to a “proxy proposal” asking for “a report on the dangers that this change might present to our insurance operation and explain how we are responding to these threats.” The good news is that the Oracle of Omaha generally takes climate science seriously. The bad news is he still doesn’t get the existential nature of the climate threat, like many in the business and financial intelligentsia, including his buddy Bill Gates, who sits on the board of Berkshire Hathaway. Buffett writes:

It seems highly likely to me that climate change poses a major problem for the planet. I say “highly likely” rather than “certain” because I have no scientific aptitude and remember well the dire predictions of most “experts” about Y2K.

It is certain that “climate change poses a major problem” for the planet, which is precisely why all of the nations of the world unanimously agreed in December to leave most fossil fuels in the ground — and the vast majority put forward serious plans to start that very process. It is “highly likely” that inaction on climate change would end modern civilization as we know it.

Especially revealing is Buffet’s choice of such a flawed analogy — comparing the risk of climate change to that of Y2K. For starters, businesses and governments listened to those who warned about Y2K and spent massive amounts of money to prevent it. Whether all or even much of that spending was warranted or not is still subject to debate. But in any case, the Y2K case is not analogous to the climate situation where inaction creates a great risk of irreversible catastrophe lasting hundreds of years — something the world’s leading scientists and governments all agree on, as explained in the latest comprehensive review of the science.

Y2K was a unique, largely untestable one

Here is how Buffett explains why he believes Berkshire isn’t threatened by climate change:

It’s understandable that the sponsor of the proxy proposal believes Berkshire is especially threatened by climate change because we are a huge insurer, covering all sorts of risks. The sponsor may worry that property losses will skyrocket because of weather changes. And such worries might, in fact, be warranted if we wrote ten- or twenty-year policies at fixed prices. But insurance policies are customarily written for one year and repriced annually to reflect changing exposures. Increased possibilities of loss translate promptly into increased premiums.

With all due respect to Buffett, climate change isn’t a limited one-time risk to Berkshire, a la Y2K, since, as we’ve seen, climate change is not like Y2K at all. It is much more like the collapse of the housing, mortgage, and financial market — an existential threat to the national and global economy, with broad and deep impacts to most Americans that can even hit a shrewd investor like Buffett hard. Had governments not intervened at the height of that crisis, we might have entered a long-lasting depression.

The similarities between climate change and Great Recession are clear if you read the book or see the movie “The Big Short,” which just won an Oscar for its screenplay. It showed how a handful of people looking at the actual data underlying mortgage-backed securities realized they were a fraud — almost the equivalent of a Ponzi scheme. They concluded there would have to be a collapse in the housing market — while the thousands of people who were causing t

he problem or should have been acting as watchdogs either were making too much money to care or were simply in denial (or both).

From a risk perspective, the key point of the similarity to climate change is that what looked in the beginning like limited risk (in just the “sub-prime” loans) turned out to be an existential risk (to the entire financial system and the economy). Buffett acknowledges:

As a citizen, you may understandably find climate change keeping you up nights. As a homeowner in a low-lying area, you may wish to consider moving. But when you are thinking only as a shareholder of a major insurer, climate change should not be on your list of worries.

The key line Buffett passes over too quickly is the one in the middle, “As a homeowner in a low-lying area, you may wish to consider moving.” Buffett is explicitly saying that homeowners in low-lying areas are at risk for losing their homes, which is another way of saying that their homes are overvalued.

While Buffett doesn’t carry that logic to its final conclusion, I did in a 2014 post, “When Will Coastal Property Values Crash”” and a 2015 post, “Florida’s Climate Denial Could Cause Catastrophic Recession.”

The key scientific point is that recent findings have led top climatologists to conclude we are headed toward what used to be the high end of projected global sea level rise this century: four to six feet or more. This means, for instance, that large parts of the East Coast would see Sandy-level storm surges almost every year by mid-century

Worse, the U.S. East Coast is very likely headed toward considerably higher sea level rise over the next century than the planet as a whole. If we don’t take very aggressive action to slash carbon pollution, we could be facing a rise upwards of 10 feet. And considerably more than that after 2100 — sea level rise exceeding a foot per decade.

And so — if we take Buffett’s one-sentence concern to its logical conclusion — we are in a major coastal real estate bubble.

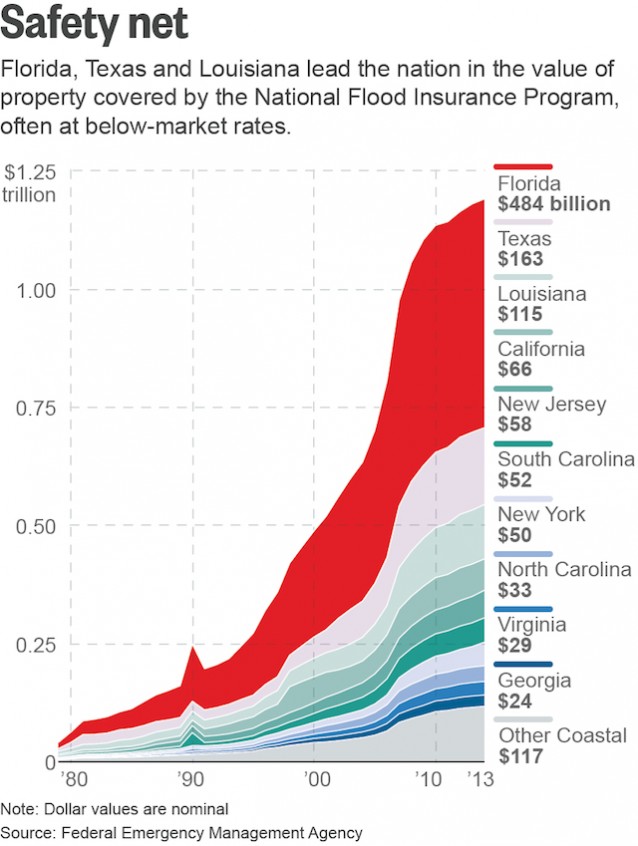

How big is the bubble, and who will pay when it bursts? The excellent Reuters series, “The crisis of rising sea levels: Water’s Edge,” has a sobering chart:

It’s a trillion-dollar bubble. And it looks like American taxpayers are on the hook for much of it. The trillion-dollar coastal property bubble will burst when a Sandy-type storm hits South Florida or those subsidies are cut or banks decide coastal property is too risky for a 30-year mortgage – or simply when the “smart money” decides it isn’t a smart investment because “we have dawdled too long.”

When does it crash, and what will that mean for the economy? On the first question, coastal property values won’t wait to (permanently) fall until sea levels have actually risen another foot or two. As I discuss in

I have no idea what the coastal property collapse means for Berkshire Hathaway shareholders. But wouldn’t it be useful for shareholders if Buffett — who has become rich being the “smart money” — discussed this in his annual letter?

Similarly, in Paris the nations of the world unanimously agreed to leave most fossil fuels in the ground. The valuation of coal companies have already collapsed. It seems inevitable that lots of companies involved in the oil business can’t sustain their huge market capitalization, especially if, as now seems entirely possible, oil demand peaks in the 2020s.

Many major institutional investors are already abandoning fossil fuel bets. Buffett himself “exited a $3.7 billion investment in Exxon Mobil Corp. amid a slump in oil prices,” at the end of 2014. But he wasn’t divesting — at the same time he was “adding to a bet on Canadian synthetic crude oil producer Suncor Energy Inc. and oil refiner Phillips 66.”

Yes Buffett is betting on the tar sands. In fact, in the third quarter of last year, Buffett “nearly doubled Berkshire’s position in Phillips 66″ — and “boosted Berkshire’s [Suncor] position by nearly seven million shares to 30 million shares, an investment now worth approximately $1.1 billion.”

So Buffett just put $240 million more into his now billion-dollar bet on the world’s dirtiest liquid fuel! Shouldn’t he tell investors of the climate risk associated with that investment in a company that can only make a big profit by helping to destroy a livable climate?

Instead, Buffett includes this lines in his letter: “Last year, BHE [Berkshire Hathaway Energy] made major commitments to the future development of renewables in support of the Paris Climate Change Conference.” I’m sorry, Warren, but you can’t place a huge bet on massive exploitation of the carbon-intensive Canadian tar sands and at the same time crow about your “support of the Paris Climate Change Conference.”

It’s also a bit strange to talk about BHE’s “major commitments to the future development of renewables” when BHE is working overtime in Western states like Nevada to kill solar energy. That hypocrisy will be the subject of my next post.